An Alternative Data Preview of the September FOMC Meeting

Key Takeaways

- MacroX, in line with the market, expects no change of policy rate at the Fed’s September meeting

- The robust labor market and lower inflation outcomes have been largely been in line with Fed projections, but strong Q3 economic data will lead the Fed to revise its growth estimate up from 1%

- Our model indicates that the market pricing of 100 bps of cuts in 2024 is too dovish, given strong growth and sticky inflation

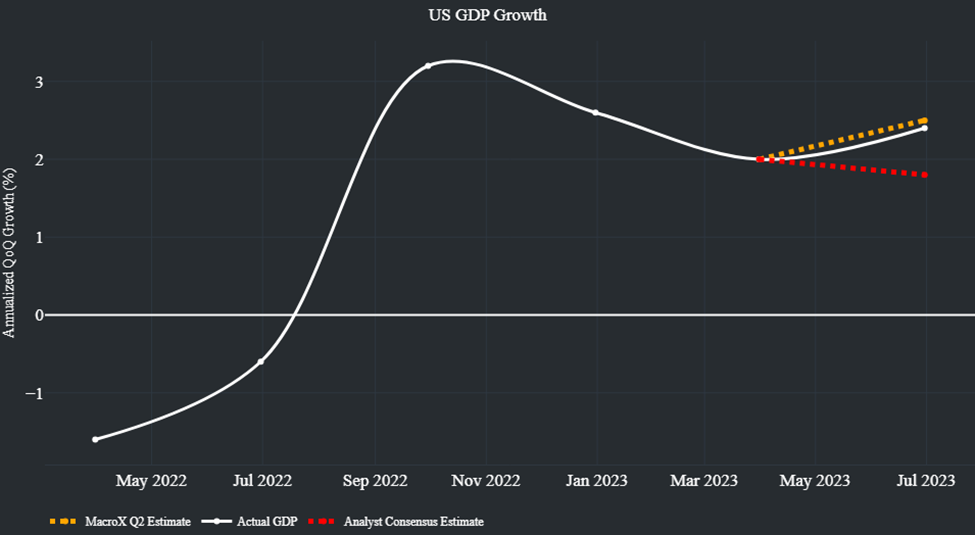

- Nowcasting has enabled MacroX to observe the strong growth in real time and call for higher rates since May, which has largely played out with the 2y higher by ~ 100 bps

Since the June Fed meeting, sentiment around the US economy has changed noticeably. MacroX’s nowcasting of US economic growth has consistently shown an economy growing faster than widely forecasted (see here, here, and here). This optimism over the US economy has now become widespread as the economic data has continually surprised to the upside. The Fed has largely signaled a desire to keep rates on hold at its meeting this week but it will also update its economic projections. Our look at alternative data-sourced measures of economic activity leads us to believe the following regarding the next set of Fed projections:

Our call for the Fed to raise their projections for future rates is based on the US economy growing at a much faster pace than expected earlier this year. The robustness of economic activity will allow the Fed to signal a slower pace of cuts next year (currently ~100bps of cuts priced into 2024). We believe a fair price for the 2024 Fed Funds Rate is closer to 5%, especially if the Fed does signal a further hike this year is more likely than not.

Growth: Accelerating in Q3

MacroX’s nowcast of US growth uses 100+ alternative data signals fed through its AI engine to generate a real-time measure of economic activity. Our nowcast of growth shows growth in the US economy meaningfully accelerated in Q3, growing at ~4%, higher than both the NYFed and Bloomberg Nowcasts but below the Atlanta Fed’s GDPNow nowcast. The acceleration that alternative data is showing is in stark contrast to the “soft data” as the Composite PMI indicated a sharp deceleration in activity in August diverging significantly from our (and other) nowcast(s).

This acceleration has been driven by an uptick in our satellite and news nowcasts. The increase in our news nowcast is well explained by the rise in positive sentiment around the US economy over the last few months (exemplified by our previous post regarding the yield curve inversion) whilst the increase in our satellite nowcast is most likely due to an uptick in industrial activity – potentially picking up the boom in manufacturing construction occurring.

The Fed projected in June for GDP growth to be 1% in 2023 and 1.1% in 2024. Official Q1 and Q2 growth has come in considerably higher than this and, given our (and other) nowcast(s) shows growth accelerating in Q3, we would expect the Fed to sizably increase their projections for growth in 2023 and 2024. Jerome Powell, in his speech at Jackson Hole last month, remarked how “growth has come in above expectations” and that “additional evidence of persistently above-trend growth…could warrant further tightening of monetary policy”.

Labor Market: Headline measures are cooling but labor demand might be ticking back up

Given the acceleration of output, the Fed could well be worried about this spilling over into a tighter labor market and thus an acceleration in wage growth. However, headline changes to nonfarm payrolls growth have been steadily slowing and the unemployment rate unexpectedly ticked up to 3.8% in August (from 3.5% in July).

Looking at LinkUp and Indeed data, we can see that job postings have fallen from their elevated level in 2022. However, there has been a slight uptick in labor demand in August.

The Fed projected the unemployment rate to be 4.1% in 2023 in June and labor market outcomes in Q3 have largely been in line with this.

Inflation: Falling but sticky around 4%

Despite inflation dropping to much more comfortable levels for the Fed over the last few months, our nowcast of inflation continues to show that a strong labor market, robust economic growth, and the end of the easing of supply conditions provide a floor for inflation with core inflation likely to remain around 4% on an annual basis over the next 3 months.

The Fed projected PCE inflation to be 3.2% in 2023 and Core PCE to be 3.9% and the latest data, coupled with our inflation projections, seem well in keeping with these outcomes. We therefore expect no major changes to these in the latest projections.

Fed Speak and Market Pricing

Our LLM-based model of Fed speak measures how hawkish or dovish the last three months of Fed communications (speeches and statements) have been and currently sees the Fed as mostly hawkish as they remain concerned over the elevated level of inflation and continue to flirt with an additional hike in November.

Interestingly our hawk/dove measure of financial news – although still predominantly hawkish – has started to tick down and has tended to lead official Fed communications over the last five years:

The market, responding to consistently better-than-expected economic data, has dramatically repriced yields higher in the months since the last Fed projections – in keeping with the views expressed by us here in May and here in June.

Given the strength of the economy and the stickiness of inflation, the 100bps of cuts in 2024 the Fed had anticipated in June seems aggressive and we expect the Fed to raise their projections for rates in 2024 and 2025 next week (with no change for rates in 2023 as they continue to leave the door open for a further hike).

MacroX has favored being paid front-end yields since early May as our nowcasts showed the US economy continuing to grow at a decent clip, well ahead of the official data (and in sharp contrast to the soft data). Much of the move higher we correctly anticipated has already occurred with rates 100bps higher since then. Given our belief that the Fed will increase their projections for future rates higher, we believe there is scope of yields to move even higher but the risks are more balanced at this time.

If you’re an institutional investor and would like access to our Nowcasting platform, sign up here to join our Waitlist.